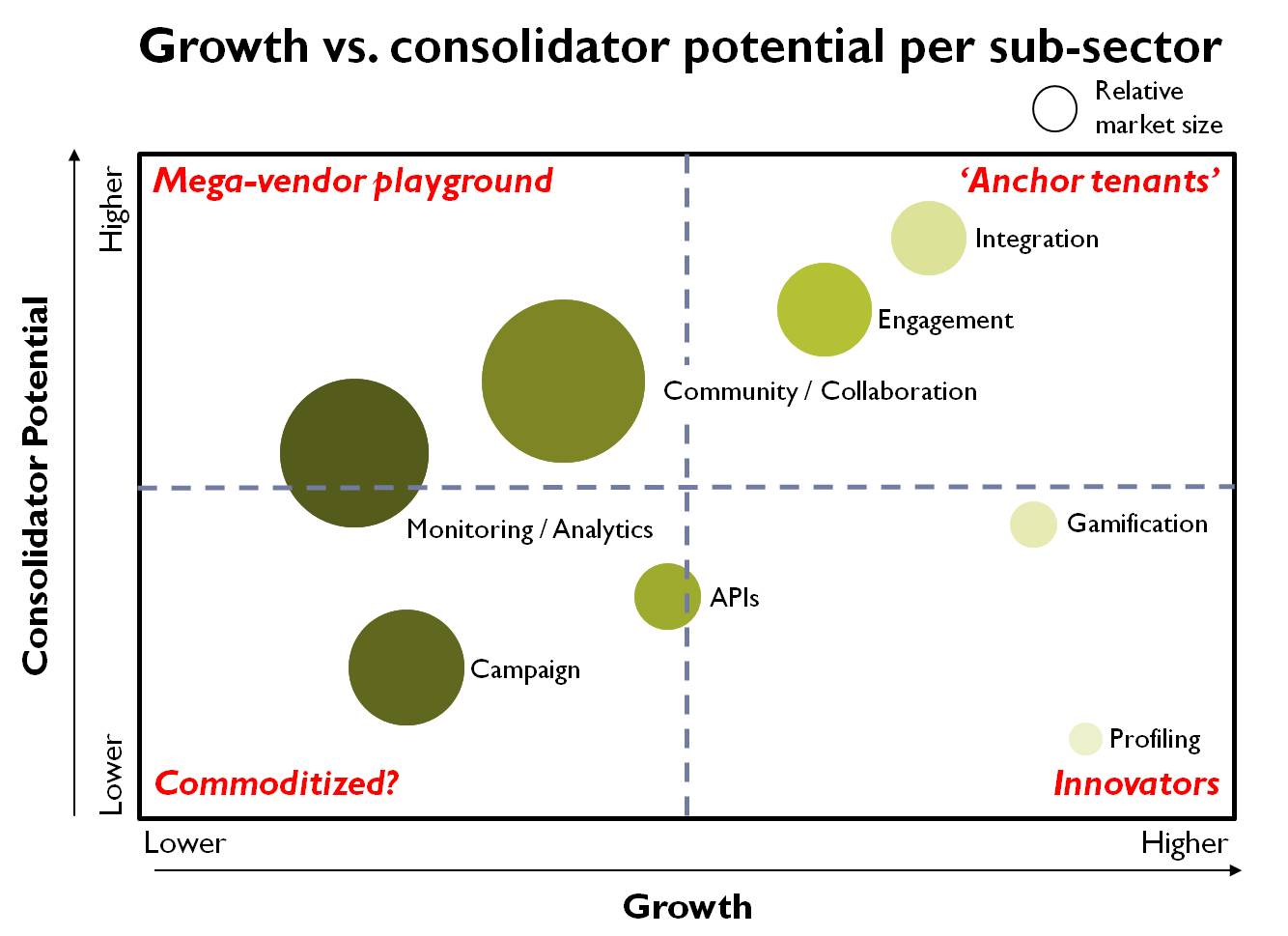

This is a follow-up post to Part 1 on the same topic. If you have not read Part 1, I suggest you start there. The chart below includes my assessment of the social enterprise software market. The size of each bubble reflects my estimate on the size of each sub-sector, while the axes represent the relative growth and ‘consolidator’ potential of each. It is not too surprising to see the most mature sub-sectors on the lower growth quadrants.  My fundamental belief is that the sub-sectors that are trying to stitch the various elements of the stack together (namely Engagement and Integration) will be the ones to watch. Please note two caveats: (i) I am not accounting for the enterprise software mega-vendors entering the market, and (ii) I am not referring to specific companies, but rather the sub-sectors themselves. As a matter of fact, I believe most companies today are present in more than one sub-sector for that very reason.

My fundamental belief is that the sub-sectors that are trying to stitch the various elements of the stack together (namely Engagement and Integration) will be the ones to watch. Please note two caveats: (i) I am not accounting for the enterprise software mega-vendors entering the market, and (ii) I am not referring to specific companies, but rather the sub-sectors themselves. As a matter of fact, I believe most companies today are present in more than one sub-sector for that very reason.

So here are the details for each sub-sector:

Profiling

These companies help their customers develop a 360o view of their own consumers by mining the social (and 1.0) web, an area historically dominated by companies such as D&B and Hoover’s. This area is critical to fulfilling the promise of SocialCRM by allowing companies to link their consumers’ digital profiles to those in their internal CRM systems. Salesforce was the first enterprise software vendor to enter this space with their acquisition of Jigsaw back in 2010. Vendors in this space fall in two categories: Companies such as Jigsaw, InsideView and Reachable that build social profiles, and companies such as Klout and PeerIndex that attempt to understand influence scores. Most capabilities in this area are still rudimentary, and companies such as Reachable are trying to improve their accuracy by leveraging internal enterprise data. I expect significant innovation in this area, although it is unclear whether it will reach maturity before getting consolidated.

Integration

While social single-sign-on integration is well understood and mature (i.e., companies like Gigya and Janrain take the pain out of the ever-changing social network APIs from their customers), other areas such as a true integration layer across the entire social enterprise software stack are rudimentary. I expect a middleware layer to emerge, akin to what happened in the enterprise software industry. I see Profiling as a potential sub-sector to be eventually subsumed into this.

Campaign

This is a very mature space, with increasing M&A activity. Five of the nine social enterprise software M&A transactions during the past 12 months were in this sub-sector. These include Buddymedia (Salesforce), Vitrue (Oracle), Involver (Oracle), and Wildfire (Google) in the past 2.5 months alone. All these companies started by providing tools to create a social network- (predominantly Facebook) and web-based campaign apps and pages, and many have since expanded to Engagement. Given that all large players have been acquired, I don’t expect much innovation in this sub-sector, beyond the acquirers’ integrating these products into their offerings.

Engagement

This sub-sector is fairly immature and crowded, but growing fast with many early-stage companies. Vendors like sprinklr, Buzzient, Spredfast, and viralheat help their customers manage their own engagement on social networks. Companies such as purechannelapps and Hearsay Social help customers with extensive franchise or partner networks. All companies in this sub-sector offer some analytics capabilities. Some, such as NextPrinciples, not only provide CRM integration but also novel ways to extract insights by providing recommendations as opposed to ‘eye-candy’ charts. I expect more innovation in this space, especially in the areas of integration and analytics.

APIs

This sub-sector emerged as a vehicle to allow full access to the Twitter firehose. A handful of companies like Gnip and DataSift have had licensed access for a while, and as of last June so has Salesforce’s Radian6. Separately, Twitter quietly announced last month they will start allowing individual users full access to their own tweets. As Twitter starts to become more serious about the enterprise, I expect them to take the brokers out of the equation.

Monitoring / Analytics

This is by far the most mature (a.k.a. commoditized) part of the social enterprise software stack, with hundreds of companies present. These companies provide capabilities for their customers to monitor social conversations. They deliver both quantitative (e.g., share-of-voice, numbers of fans/followers, engagement metrics), and qualitative (e.g., sentiment) metrics. Salesforce was the first enterprise software mega-vendor to enter this space with its acquisition of Radian6 in 2011, and Oracle acquired Collective Intellect last month. By now, most companies in the adjacent Engagement sub-sector provide varying degrees of listening and monitoring capabilities. Although some vendors in this sub-sector tried to provide publishing and engagement capabilities, none have really succeeded to date. I expect further consolidation and limited innovation in this area as other large enterprise software companies enter this ‘table-stakes’ space.

Gamification

This emerging area within the social enterprise software stack is currently dominated by two companies, Badgeville and Bunchball. These companies provide capabilities to influence consumer behavior by using concepts borrowed from the gaming industry. In all cases, these capabilities are exposed through their customers’ own websites or communities. For more information on gamification read this report by Ray Wang of Constellation Research, or visit this site managed by Mario Herger of SAP. Other players across the stack have already started to incorporate gamification components into their offerings. I expect this sub-sector to be absorbed, most likely within the Integration layer.

Community / Collaboration

Companies in this sub-sector provide capabilities to develop private communities (akin to the public / open social networks). They vary from full-blown platforms like Jive and Lithium to the more targeted / micro-blogging platforms like Salesforce’s Chatter and Microsoft’s Yammer. This is a fairly mature sub-sector that boasts the only pure-play public company (Jive went public last December) and largest social enterprise software acquisition to date (Microsoft acquired Yammer for $1.2 billion last June). By now, almost every enterprise software mega-vendor has some capabilities, given the relevance of these capabilities to their customers’ core business processes. Most, however, fall short of that integration promise today. I expect most innovation in this area to come from the large enterprise software vendors as they try to integrate the capabilities to their core business process offerings.

As I mentioned in my previous post, the innovation and expected growth for the social enterprise software market will continue at a breathtaking pace. I look forward to revisiting this topic a year from now. In the meantime, your thoughts and feedback are more than welcome as this is still work-in-progress.

[…] (August 15): You can continue to Part 2 here. var dd_offset_from_content = 40; var dd_top_offset_from_content = 0; […]